Shell was the world’s largest user of carbon credits in 2024, a year in which fossil fuel companies dominated the voluntary carbon market. This allows them to pretend they are taking significant climate action, while continuing with business as usual.

Since the ratification of the Paris Agreement, companies have shifted the way they consider and tackle climate change. This trend is reflected in the growing number of companies engaging in environmental initiatives and setting climate commitments. However, many companies use carbon credits from the voluntary carbon market to offset their emissions or reach climate targets on paper, including some of the most polluting, as NewClimate Institute and Carbon Market Watch have uncovered in multiple editions of the Corporate Climate Responsibility Monitor.

Unfortunately, this phenomenon has weakened the climate mitigation efforts outlined in the Paris Agreement by providing a double gimmick for big polluters. On the one hand, offsetting emissions allows companies to cheaply sidestep costly internal decarbonisation efforts. On the other hand, it gives them a powerful marketing tool to greenwash their image while weakening the case for stronger regulatory action.

Playground for polluters

In recent years, both the demand for and supply of carbon credits have increased, though there has been a downturn since 2022, partly due to serious quality shortcomings and scandals that have rocked the market. In 2024, around 255 million credits were issued and 162 million were used (“retired”, in market terminology), mostly from avoided deforestation (REDD+) and renewable energy projects. The financial sector and energy sector were tied as the largest cohort of buyers, with the energy sector coming out on top in terms of credits retired in 2024, according to data from Allied Offsets.

The biggest purchaser in 2024 was Shell, which used up 14.1 million carbon credits – with more than half used in December alone – which represented almost three times the number of credits used by the next biggest buyer, Microsoft. Shell prominently uses carbon credits to greenwash its liquefied fossil gas as “carbon neutral LNG”, including through scandal-hit projects the company is associated with but for which it appears to refuse to accept liability.

Other prominent buyers from the oil and gas sector in 2024 – according to Carbon Pulse – were Eni, which used around 6 million credits, with the explicit aim of increasing their use of offsetting to reach their climate targets, followed by Engie (2.1 million), Woodside Energy (1.4 million) and PetroChina (1.2 million).

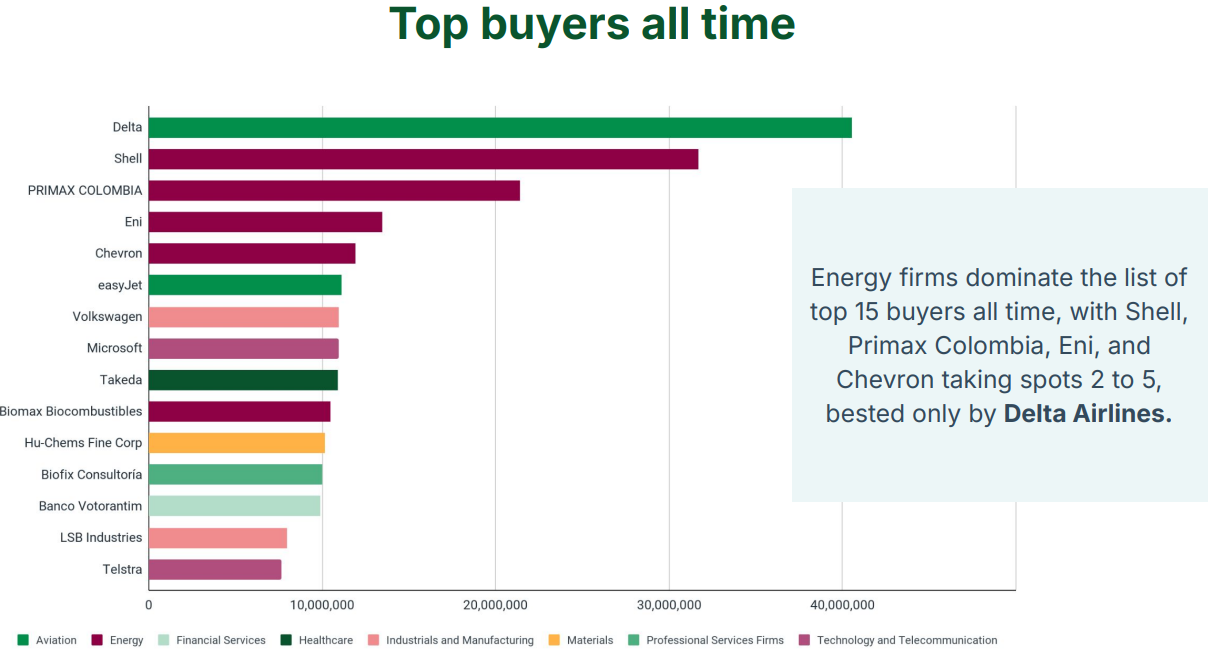

Strikingly, eight out of the 10 top buyers of carbon credits of all time, where there has been disclosure, are from heavily polluting industries: energy, aviation, and automotive (see graph). While Delta, the largest buyer of carbon credits to date, stepped away from the market in 2022, some of the world’s largest airlines appear to be increasingly entering the market; despite the legal risk this may entail.

Note: reproduced with permission from Allied Offsets (2025), “VCM 2024 Review Emerging Trends for 2025”

Black box

Companies may be using far more credits than are being disclosed due to a lack of transparency in voluntary carbon market registries. The main voluntary standards do not currently require public disclosure of who used the carbon credits or their reason for doing so, such as to offset emissions. This information is only made public if the final buyer requests it. This means that we have an incomplete picture of the role the voluntary carbon market plays.

This transparency loophole in the VCM needs urgent fixing. Given that the Integrity Council for the Voluntary Carbon Market (ICVCM) has a requirement for carbon crediting standards seeking its seal of approval to disclose such information (criterion 2.1), one would expect the ICVCM-approved standards to implement this practice. This does not yet appear to have been implemented by the main standards, raising questions for ICVCM about how loosely it enforces its own requirements.

Junk credits

The transparency issue goes hand in hand with quality concerns that have rocked the market.

More evidence of the low quality of many carbon market projects continues to emerge. Much of the scrutiny from researchers and civil society has focused on the project types making up the bulk of the VCM. These include nature-based projects, such as REDD+ which is prone to over-crediting, and renewable energy projects, which often bring no additional climate benefits that would not have occurred otherwise.

Seeing the forest for the trees

The fact that most credits in the voluntary carbon market – the bulk of which emanate from the lower end of the quality spectrum – are purchased by the oil and gas sector merits serious reflection as it challenges the commonly held belief that companies active in the VCM are climate leaders.

The narrative that companies purchasing carbon credits are also more ambitious in their internal decarbonisation is a convenient one for heavy polluters but lacks any causal evidence. Studies from Sylvera, MSCI (formerly Trove Research), and Ecosystem Marketplace indicate a potential correlation between the two but crucially do not establish a causal link. Yet, these studies are often used by many market players to imply that the purchase of credits, often for offsetting purposes, leads to greater internal decarbonisation.

In fact, recent research (currently in pre-print) contests the messaging around these studies, even finding that the purchase of carbon credits may compete with financing for internal decarbonisation in the cases of Delta and easyJet. The Science Based Targets initiative (SBTi) also recently concluded “that there could be clear risks to corporate use of carbon credits for the purpose of offsetting [including] potential unintended effects of hindering the net-zero transformation and/or reducing climate finance.”

Let’s also not forget that the oil and gas sector has critically inadequate climate pledges. The renewed prioritisation of profits and returns to shareholders over internal decarbonisation efforts remain constant themes for the sector. For instance, Shell urged its shareholders to vote down a resolution brought by the Dutch NGO Follow This for the oil giant to align its decarbonisation targets with the goals of the Paris Agreement, which was ultimately rejected. On a similar note, British Petroleum (BP), which is also controversially active in the VCM, recently backpedalled on its climate target in favour of a “more pragmatic” approach – a common trend in the oil and gas sector.

Finally, fossil fuel companies are deeply involved in multiple aspects of the carbon market, raising questions around potential conflicts of interest. In addition to being among the biggest buyers of carbon credits, they are also involved in generating credits (as project developers). Take, for instance, Shell’s investment in CarboNext, a Brazilian carbon credit developer, BP’s ownership of US-based Finite Carbon, one of the largest project developers (highest issuance in VCM in 2023), and Occidental Petroleum’s acquisition of direct air capture company Carbon Engineering which it sees as a way to “give [the oil and gas] industry a licence to continue to operate for 60, 70, 80 years”. Many also have their own trading desks, serving as brokers. Big Oil also actively participates in VCM conferences and discussions, and even has representation in initiatives that play a key role in shaping the credibility of the market.

While there can be a role for carbon credits, possibly as part of a company’s beyond-value chain mitigation approach without any use of offsetting, let’s not be under any illusions about the way the VCM is predominantly used by the petroleum sector and other heavy polluters to mislead the public and distort corporate climate ambition. In a year where various standards bodies – such as the Science Based Target initiative (SBTi), the GHG Protocol and the Voluntary Carbon Markets Integrity initiative (VCMI) – will all weigh in on the role, if any, of carbon credits in corporate strategies, let’s not forget to see the forest for the trees.